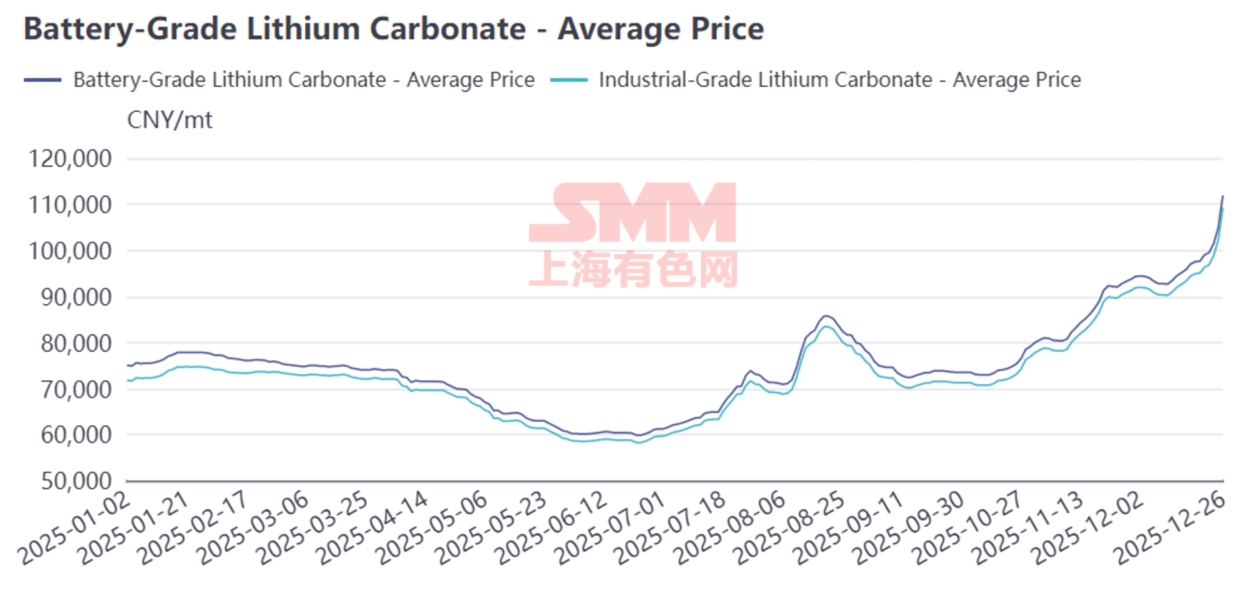

Price Review

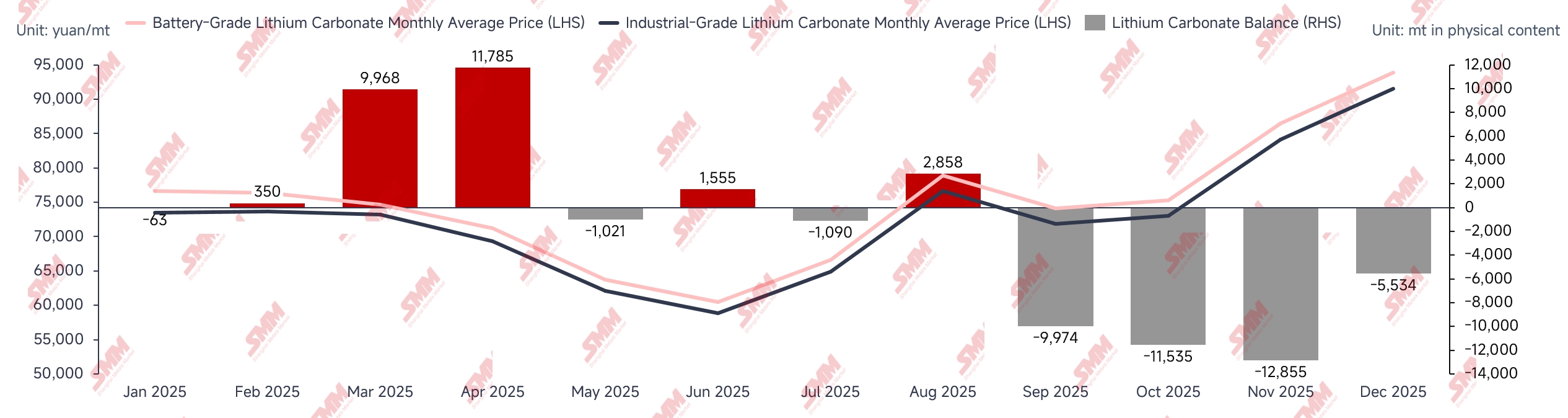

2025 H1: Following the Chinese New Year, the resumption and ramp-up of production at leading mines and salt plants in Jiangxi led to a significant monthly surplus of lithium carbonate. This substantial surplus dragged down spot prices, while capital sentiment flowing into the futures market caused an oversold situation in H1, with the price of lithium carbonate falling to a low of below 60,000 yuan/mt. Non-integrated lithium chemical plants faced immense pressure from losses, leading to widespread production cuts or suspensions, shifting the market from a significant monthly surplus to a tight balance.

2025 H2: EV and ESS sectors grew beyond expectations, driving continuous increases in production schedules for battery cells and cathode materials. Although this also boosted the operational enthusiasm of lithium chemical plants, reduced lithium resources in Jiangxi and Qinghai resulted in the growth rate of lithium carbonate supply failing to keep pace with demand growth. In H2, monthly balances for lithium carbonate showed sustained significant destocking, with prices rebounding from the bottom and the upward trend continuing.

Supply-Side Review

SMM Domestic Lithium Carbonate Production Review

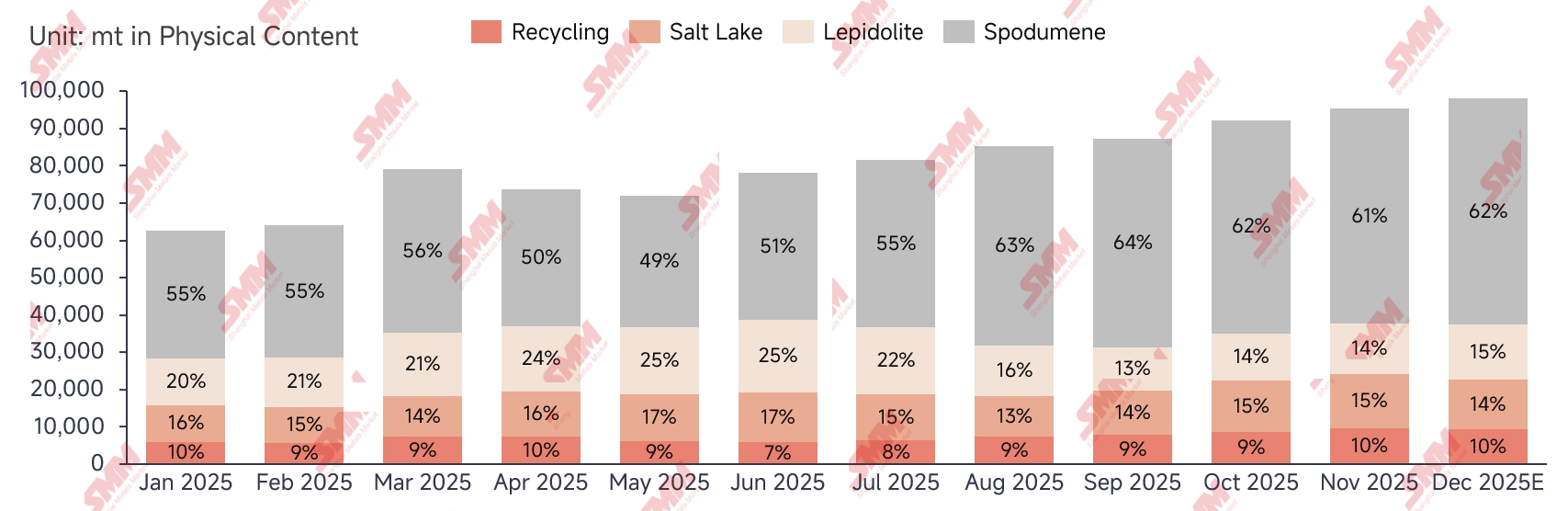

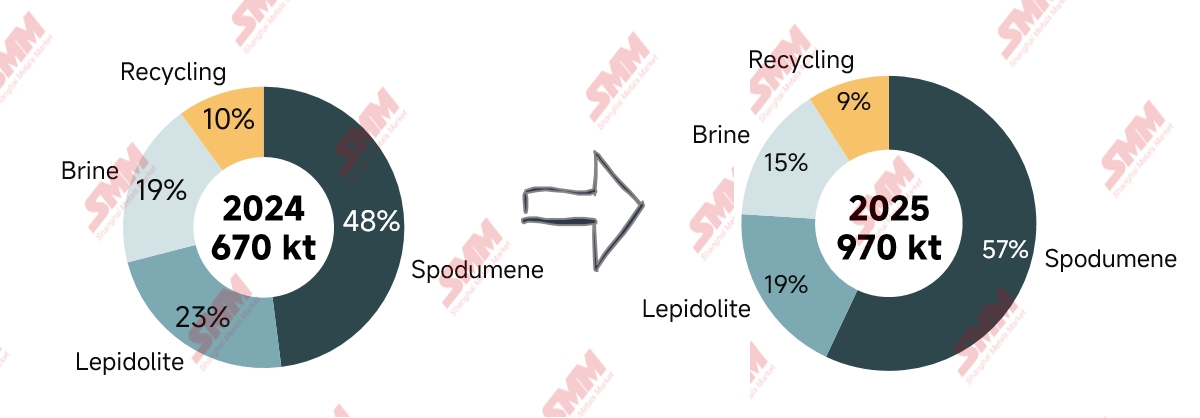

In 2025, SMM's domestic lithium carbonate production reached approximately 970,000 mt, a significant increase of 43% YoY. At the beginning of the year, monthly output remained at a low level for the year due to concentrated maintenance at lithium chemical plants. After the Chinese New Year, demand recovered, coupled with the resumption of production at leading mines and salt plants in Jiangxi, leading to a sharp rise in monthly output to 80,000 mt. Subsequently, due to an excessive decline in lithium carbonate prices, non-integrated lithium chemical plants suffered severe losses and significantly cut production, causing monthly output to continue contracting. It was only after several rebounds in the futures market spurred hedging demand that production gradually recovered. In H2, significant supply reductions occurred in Jiangxi and Qinghai. However, as lithium carbonate prices stopped falling and rebounded, coupled with stronger-than-expected demand growth, spodumene-derived production enthusiasm surged, offsetting the reductions in Jiangxi and Qinghai. Monthly output continued to break new records, approaching the 100,000 mt mark. By raw material, spodumene-derived lithium carbonate showed notable growth, with output surging 70% YoY, and its proportion approaching 60%.

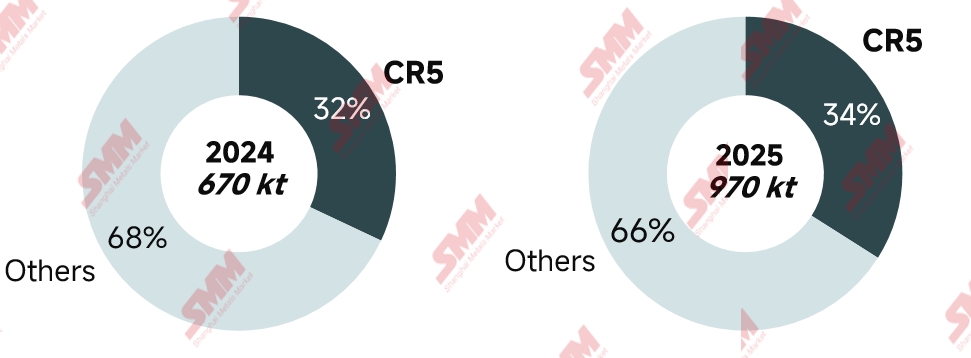

From the current changes in the CR5 market share, the industry concentration of lithium carbonate enterprises remains relatively small, with numerous participants in the sector. Leading first- and second-tier lithium chemical plants have undertaken certain capacity expansion actions this year, but the overall CR5 market share shows little change compared to last year.

Overseas Imports

According to customs data, China's lithium carbonate imports in 2025 amounted to approximately 250,000 mt, up 9% YoY. Chile and Argentina remained the primary sources of lithium carbonate imports for China, with imports from Chile totaling about 150,000 mt, down 17% YoY, accounting for 60% of China's total imports; imports from Argentina reached approximately 70,000 mt, up 56% YoY, representing 28% of total imports; imports from Indonesia were about 6,000 mt, primarily produced by Chinese lithium chemical enterprises with overseas operations, accounting for 2% of China's total imports.

Although shipments of lithium carbonate from Chile to China decreased YoY, shipments of lithium sulfate increased significantly. Chile's lithium sulfate shipments to China in 2025 were approximately 90,000 mt in physical content (conversion to lithium carbonate equivalent varies per batch due to differing lithium content), up 29% YoY.

On the export side, China's lithium carbonate export share is relatively small, and overall overseas demand growth is currently sluggish. Overseas salt lake-derived lithium carbonate production holds a relative cost advantage. In 2025, China's lithium carbonate exports were less than 5,000 mt.

Demand Side Review

EV Market

The global NEV market maintained growth amid regional divergence in 2025, with global NEV sales expected to reach approximately 20 million units, up 17% YoY. The Chinese market continued to lead, accounting for over 70% of global sales, supported by a well-established supply chain and sustained consumer demand, transitioning from "scale expansion" to "structural upgrading" with a YoY growth rate exceeding 20%. Europe achieved steady growth, driven by high regulatory standards and localization policies, with a YoY growth rate of around 10%. However, subsidy tightening and deepening trade barriers intensified market competition. In the US, influenced by adjustments to the One Big Beautiful Bill Act (OBBBA), new energy incentives weakened, the competitiveness of conventional fuel vehicles rebounded, and the passenger NEV market experienced a YoY decline. Overall, the global NEV market in 2025 exhibited a pattern of "slowing growth but a solid foundation," with regional policy differences reshaping the future industry chain layout.

ESS Market

The global ESS market performed remarkably in 2025, with global battery cell shipments expected to exceed 550 GWh, representing a YoY growth rate of nearly 80%. Demand surged in multiple regions. The momentum of the Chinese ESS market continued to strengthen, while the Middle East, Australia, and Southeast Asia also delivered impressive market performances driven by favorable policies, somewhat diluting the demand share of the US and Europe.

By region, the Chinese ESS market initiated a critical transition from mandatory energy storage allocation to market-oriented operations, driven by the guiding policy "Document No. 136". Subsequently, "Document No. 394" and "Document No. 411" were issued, paving the way for ESS commercialization by establishing a national unified electricity market and enriching revenue mechanisms. Inner Mongolia achieved explosive market growth, becoming a significant growth driver for the year, leveraging unprecedented capacity subsidy policies and the "New Energy Doubling Plan" (targeting 150 GW of renewable energy installed capacity by 2025). Overall, the Chinese ESS market delivered a remarkable performance in 2025 on a high base, supported by local policies during its market-oriented transition. US demand fluctuated due to repeated changes in tariff policies, leading to an export rush phenomenon that persisted until October. This rush finally subsided as US-China tariff negotiations set the tone for tariff policies for the coming year. The European ESS market underwent a structural shift under the dual influence of clear policies and unexpected events, collectively stimulating a concentrated outbreak and strong growth in household ESS demand this year. Cathode Material

In 2025, SMM estimates China's total LFP production at approximately 3.75 million mt, up 60% YoY. Driven by stronger-than-expected demand growth in the EV and ESS markets, the increase in domestic LFP output was concentrated in H2. Nearly 20 leading first- and second-tier enterprises were operating at full capacity, while orders and toll processing volumes for small and medium-sized enterprises also rose significantly, pushing the industry's operating rate above 70%. In terms of product structure, high-compaction products continued to gain penetration, with the share of 4th-generation high-compaction LFP in total production rising to 10–15%, though supply of high-compaction capacity remained tight.

In 2025, SMM estimates China's total ternary cathode material production at around 820,000 mt, up nearly 20% YoY, mainly benefiting from the rapid volume expansion of mid-nickel high-voltage materials and strong growth in the small power market. Currently, overcapacity in domestic ternary cathode material is prominent, with the average industry operating rate expected to be only 45% in 2025. Against a backdrop of intensifying competition and limited market growth potential, further expansion of domestic ternary cathode material capacity is highly unlikely.

Supply-Demand Balance and Inventory

In 2025, domestic lithium carbonate experienced a rare destocking pattern, with the annual destocking volume reaching approximately 10,000-20,000 mt.

H1 2025: After the Chinese New Year, with production resumptions and ramp-ups at leading mines and salt plants in Jiangxi, lithium carbonate experienced a significant monthly surplus. This substantial surplus dragged down spot prices, while capital sentiment flowing into the futures market caused an oversold price situation in H1. Non-integrated lithium chemical plants faced huge losses under pressure, leading to widespread production cuts or suspensions, shifting the significant monthly surplus to a tight balance.

H2 2025: EV and ESS growth exceeded expectations, driving continuous increases in production schedules for battery cells and cathode materials. Although this also boosted the operational enthusiasm of lithium chemical plants, reduced lithium resources in Jiangxi and Qinghai meant the growth rate of lithium carbonate supply could not keep up with demand growth. In H2, lithium carbonate's monthly balance showed continuous and significant destocking.

Lithium carbonate inventory in 2025 showed an evolution characterized by "accumulation first, then destocking, with structural shifts." In H1, due to lithium chemical supply growth significantly outpacing downstream demand, coupled with an increased proportion of long-term agreements, downstream material plants had low purchase willingness for spot orders, leading to continuous inventory accumulation in the upstream segment, with its proportion remaining around 45%. In H2, end-use demand for EV and ESS exceeded expectations. Despite continuous increases in upstream supply, it still struggled to meet robust demand. This caused inventory to shift rapidly from upstream smelters to material and battery segments, with the upstream inventory proportion gradually pulling back to around 20%, entering a rapid destocking phase. As lithium chemical supply remained tight and demand continued robust, both upstream and downstream showed synchronized destocking, with upstream destocking being more significant. The total industry days of inventories have now fallen to below one month.

2026 Supply-Demand Outlook

The global passenger NEV market will transition from "sales expansion" to "structural optimization and regional balance." New energy commercial vehicles will also enter an accelerated volume release phase, driven by policy support, cost inflection points, and maturing application scenarios. Overall, global NEV sales in 2026 are expected to maintain a growth rate of around 15%. In 2026, China's ESS capacity subsidies will decline slightly but remain economical, while overseas AIDC scenarios release incremental demand. ESS battery cell demand will continue its high growth trajectory. From the supply side, new capacity additions next year will mainly be large cells, but market acceptance of large cells will still require time. Therefore, the market in 2026 will still be dominated by the 314 product as the main product. This leads to a situation where capacity cannot keep up with supply amid high ESS demand, maintaining a tight supply-demand balance in the ESS market. ESS battery cell production growth in 2026 is projected to be between 30% and 40%.

Supply side, global lithium carbonate production will exhibit a pattern of "high total volume, slowing growth rate, and structural divergence." Incremental space will mainly come from new investments and expansions in integrated capacity, with the YoY growth rate expected to reach about 30%. If future demand grows beyond expectations, against the backdrop of limited short-term expansion in lithium chemical capacity, tight supply will push the price center upward, thereby bringing more overseas lithium carbonate into the domestic market. Simultaneously, price increases will also accelerate the release of flexible increments in lithium resources and lithium chemical capacity. Once tight supply gradually eases, price increases will also be constrained. In the future, the market will gradually move towards balance through dynamic adjustment between "price and supply."